(but Bill also increases the tax rate)

On Wednesday May 21, Governor Bob Furgeson signed Engrossed Substitute Senate Bill 5813 which increases the Washington Estate Tax Exemption and Rates; Washington Capital Gains; and Addition of Qualified Non-Familial Heir for QFOBI

Highlights:

- New law goes into effect on July 1, 2025, for WA Exemption and tax rates

- WA Exemption will increase from $2,193,000 to $3,000,000

- Annual inflation adjustments to the WA Exemption will begin on January 1, 2026

- Estate tax rates will increase from a top rate of 20% to a top rate of 35%

- Starting January 1, 2025, an additional 2.9% on long-term capital gains over $1,000,000

- Definitions of “qualified non-familial heir” and “employee of a farm” added for QFOBI

The Details:

Washington Estate Tax Exemption and Rates

Washington Exemption and Tax Rates before July 1, 2025: Before the bill was signed, the exemption from estate tax was $2,193,000 per person and this amount has been frozen since 2018. The $2,193,000 WA Exemption remains in effect until July 1, 2025.

The old tax rates range from 10% to 20% on estates that exceed $2,193,000:

WA Exemption and Tax Rates on or after July 1, 2025: Starting on July 1, 2025, the new WA Exemption will be $3,000,000. The WA Exemption will be adjusted annually for inflation, starting on January 1, 2026.

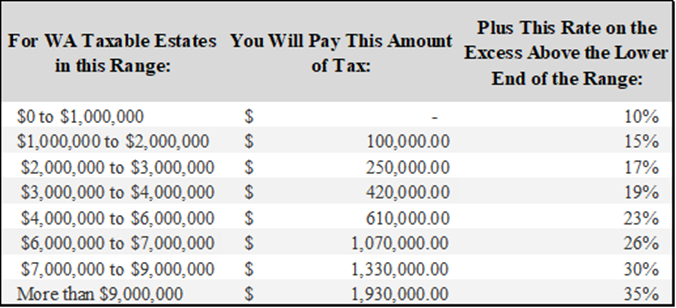

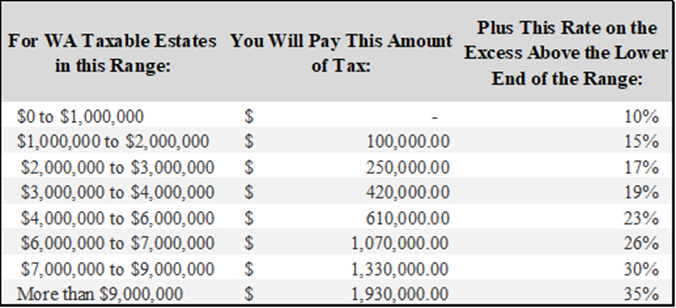

The Washington State Legislature also increased the estate tax rates. Starting on July 1, 2025, Washington estate tax rates will range from 10% to 35% on estates that exceed the WA Exemption:

Washington Capital Gains Tax

A 7% excised tax is imposed in Washington on long-term capital gains that exceed a $270,000 standard deduction. Starting January 1, 2026, for long-term capital gains that exceed $1,000,000 an additional 2.9% excise tax is imposed. No changes were made to existing exemptions from the long-term capital gains excise tax.

Farm Employee – Qualified Non-Familial Heir

Additional definitions of “Employee of a farm” and “Qualified nonfamilial heir” were added. This means that individuals who are not family members, but who are deemed “qualified,” can benefit from the QFOBI deduction when inheriting a family-owned business interest.